More than 8,000 industry professionals came together to network, learn and connect at the 2024 Wholesale & Specialty Insurance Association (WSIA) Annual Marketplace in San Diego in September. Once again, the Risk Placement Services, Inc. (RPS) leaders met onsite with carrier and business partners to discuss opportunities and trends heading into 2025, with a key focus on transportation, property, casualty, executive lines, small business and healthcare. Energy was high throughout the week as we shared conversations about the dynamics of the excess and surplus (E&S) market.

As always, market rates and trends topped the agenda of each meeting at WSIA. Now that we're in Q4 and approaching end-of-year renewals, it's timely for you to meet with experts at RPS for details on the market as discussed at WSIA.

Here are key takeaways from the biggest industry event of the year, including actions to consider taking now.

1. Transportation Industry Navigates a Challenged Economy

Ample discussion about profitable growth proves that it's still a focus for carriers as they grapple with the challenges of social inflation and litigation funding. It's clear that we need more advocacy to find a comprehensive solution, even with some state legislations addressing these issues.

It's also clear that the industry is navigating the effects of the US economy — monitoring the rising cost of auto and fleet repairs and any increases in theft that historically occur in challenging economies. Carriers shared that they'll remain vigilant and implement robust security measures to protect their assets and mitigate potential losses.

Carriers shared that they'll continue to request — and in some cases require — increased telematics and client data sharing. Telematics programs that include cameras in trucks and provide electronic logging device (ELD) information to insurance providers not only can reduce upfront costs but also enhance future operational safety.

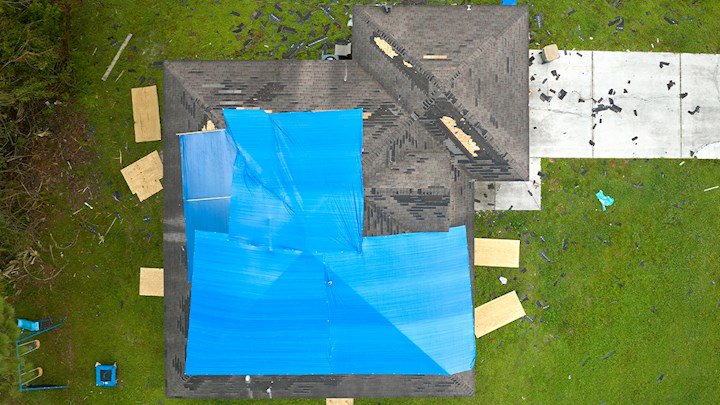

2. Property Experts Monitor Severe Convective Storms

As we reported in the 2024 Q3 State of the Property Market report, the market was a main focus, and we've quickly propelled into a buyers' market that's created a much-needed reprieve for insureds and a lot of frustration among insurance carriers with deteriorating market conditions.

Carriers reported that severe convective storms peril remains problematic, with wind and hail claims as a key driver.

3. Casualty Remains the Hottest Topic of Discussion

As we expected, conversation continued about the "predictably unpredictable" market, as we reported in our 2024 Q3 Umbrella and Excess Market Update. We'll be diving more into the dynamic casualty market in our upcoming Q4 report.

4. Small Businesses Eye Talent Development for Growth

Throughout the week, we continued to hear more conversation about deductibles as a tool to help manage loss performance versus rate increases. But turnaround time and speed are more important than ever.

During our meetings, we heard from carriers that talent is crucial for growth. Companies that attract talented individuals experience faster growth than those struggling with recruitment. Educating teams and partnering with younger members both are key strategies to achieving the desired growth.

5. Healthcare Carriers Are Looking to Diversify

Healthcare carriers shared that they continue to be pleased with their growth in the E&S space. Some carriers are considering entering the behavioral health space as well, strictly for wholesale distribution.

6. Take Action and More Control in Client Conversations

Discussions emphasized the importance of partnering with carriers and wholesalers with the experience to understand clients' specific business and needs to ensure that clients have the proper coverage in place at the time of a claim.